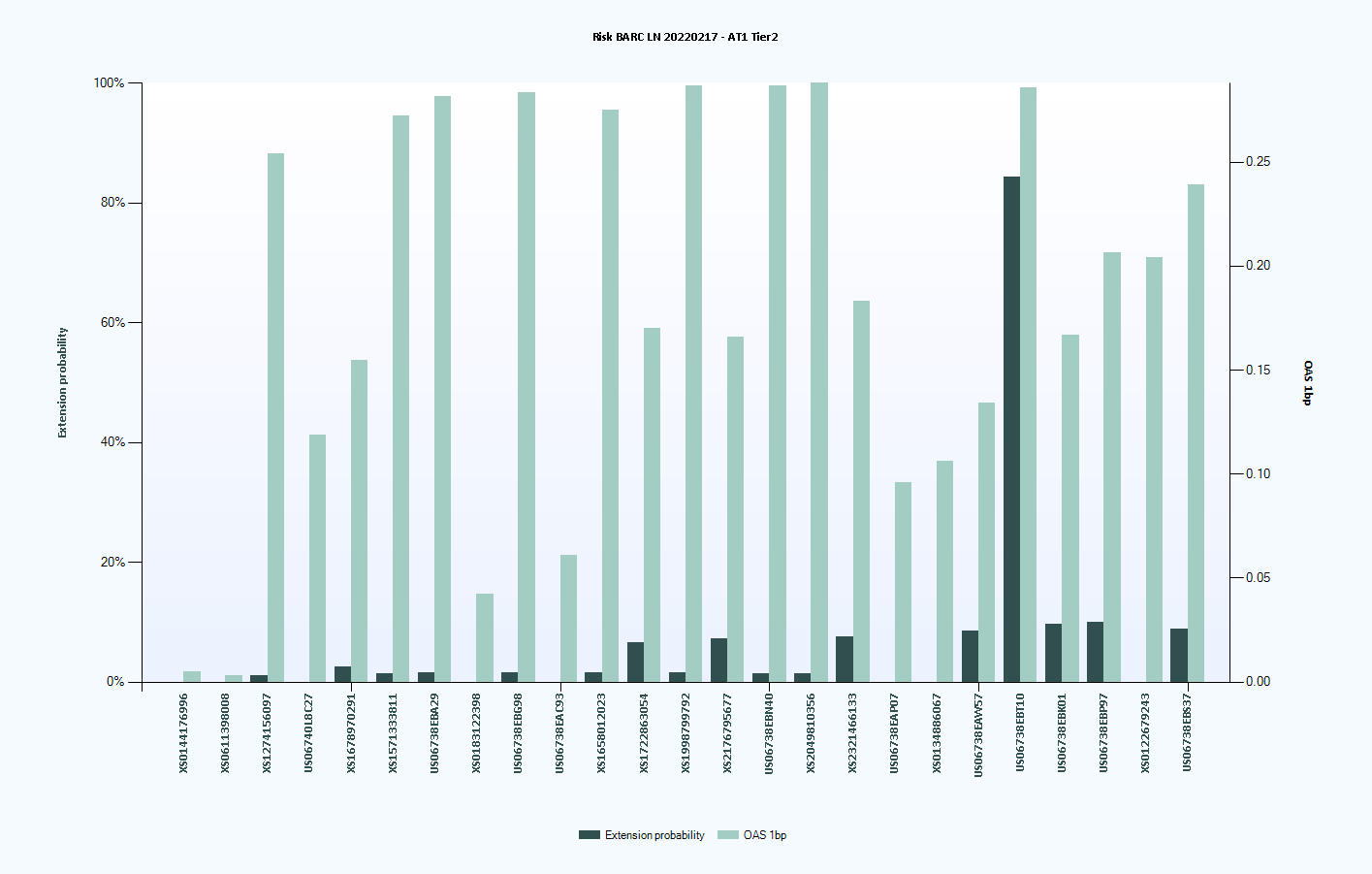

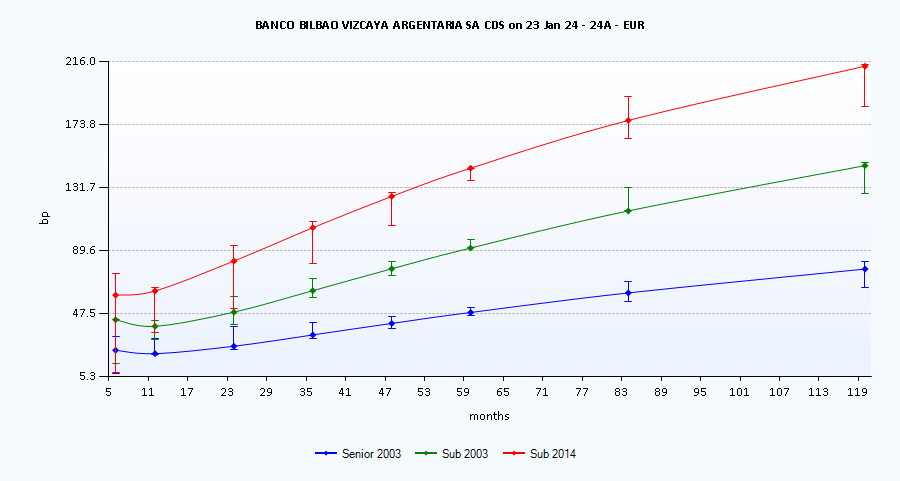

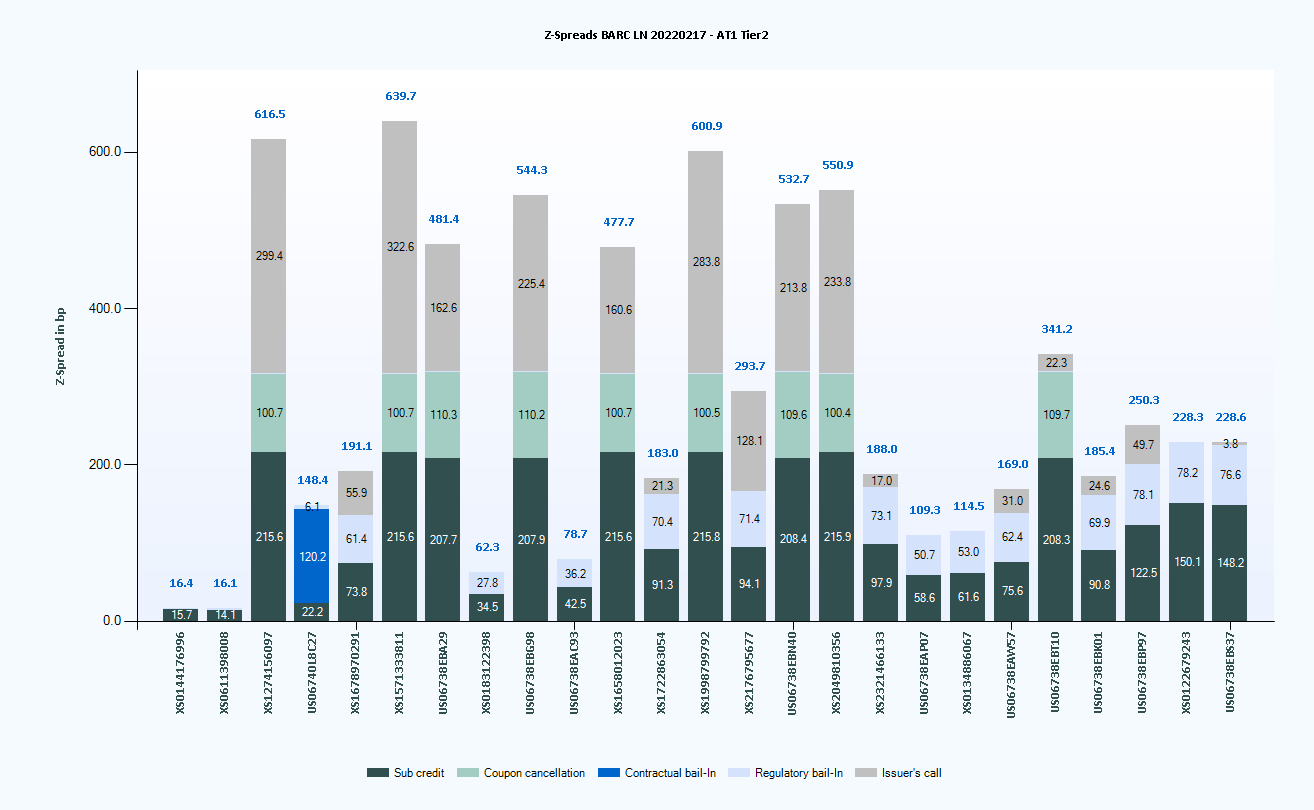

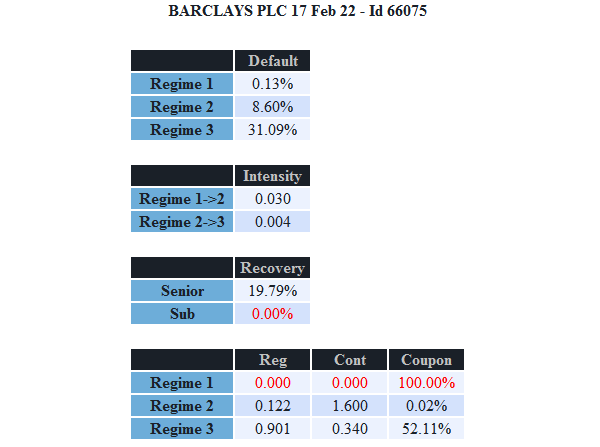

CoCo33 draws its robustness from a unique feature: its model is calibrated on all the relevant instruments related to an issuer. For a bank, those instruments include the AT1 bonds or preferred shares, the Tier 2 bonds, and possibly the subordinated or senior CDS following the ISDA 2003 or 2014 definitions. Once the model is calibrated, it is possible to infer a wide range of risk statistics and to assess if a security is relatively cheap or expensive.

31 RUE FROIDEVAUX 75014 PARIS, FRANCE

31 RUE FROIDEVAUX 75014 PARIS, FRANCE

If you prefer send us an e-mail

If you prefer send us an e-mail