The following news and events will help you navigate through ITO33

and provide information about our activities and events.

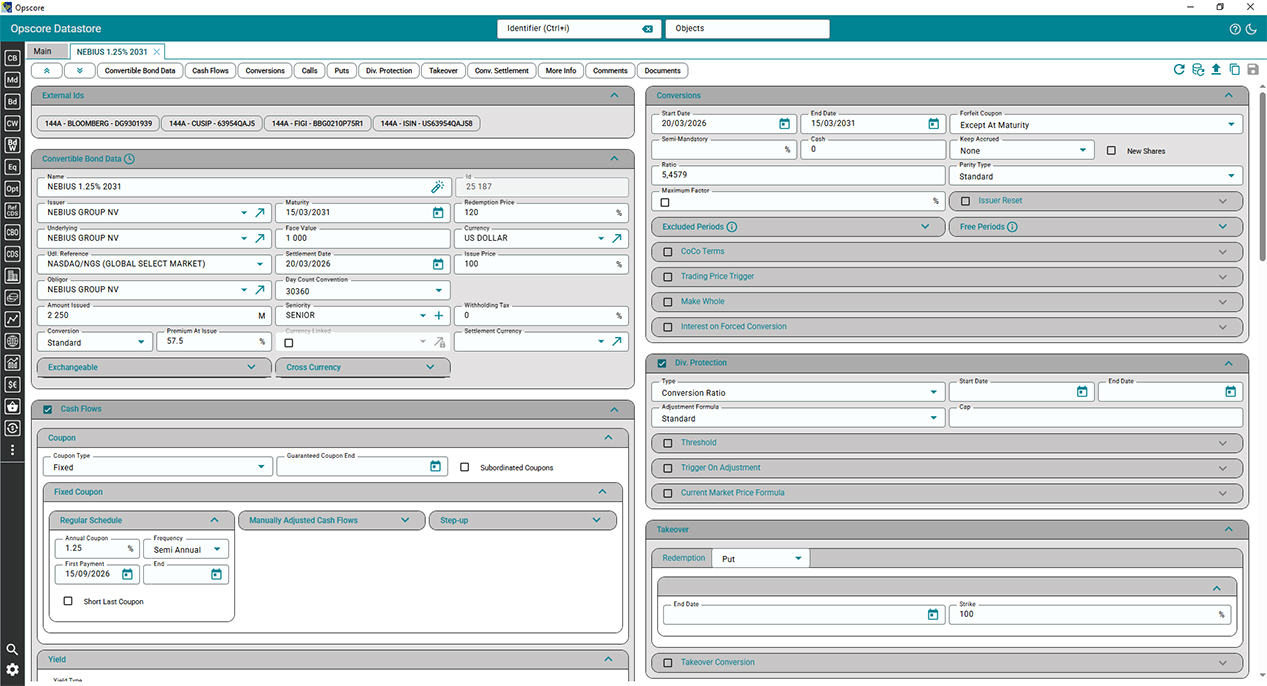

Opscore 3.9.7.0 brings a range of new capabilities, including new features and important updates to end-users, such as:

A changelog document presenting the list of all changes (FrontEnd, Pricing, XLL, Interface, DB Edit) is available on request.

We highly recommend updating to the latest version to take full advantage of these improvements.

ITO33 is pleased to announce the release of IssueConvertibles, a stand-alone Convertible Bond Pricing solution designed specifically for ECM users. IssueConvertibles provides a user-friendly interface to quickly set-up and evaluate a new issue, handling complex terms to help meet the issuers requirements. Main functionalities include scenario analysis on a range of coupons and premiums, volatility and credit assumptions, generation of watchlists to help compare different structures over time for optimal timing of launch, new issue reports and several other helpful features.

We have positive feedback from current users and other institutions trialling.

ITO33 is pleased to announce that two new major institutions have selected CoCo33 valuation and risk management solution to oversee and manage their holdings of regulatory capital securities such as AT1 bonds, Tier2 bonds and RT1 bonds. Other institutions are currently evaluating our model and the pipeline looks promising.

ITO33 is glad to invite portfolio managers and risk analysts to a presentation of CoCo33, our pricing and risk management solution for regulatory capital securities issued by banks and insurance companies.

Date: April 4, 2024

Time: 4:30pm

Venue: Le Bristol, 112 rue du Faubourg Saint Honoré, Paris

Speakers: Philippe Henrotte, Co-Founder and partner of ITO33, Head of Research and Willy Lorange, Head of Quant Support Team.

Presentations finish at 18:30 and will be followed by drinks and canapes.

To attend, please submit your details by filling the Contact Us form.

We will be thrilled to welcome you on the 4th of April.

The ITO33 team

Most notably:

Opscore 3.9.6.0 delivers several new capabilities to end-users:

CoCo33 Data Service delivers to risk managers consistent pricing and risk data on Regulatory Capital Securities issued by Banks and Insurance companies.

ITO33 is Sponsor of Quant Insights conference: THE CASE OF BANK REGULATORY CAPITAL SECURITIES

27th-28th October 2021, Globally Live-Online

Paris, May 11, 2020 - ITO33 announces a new major version of Opscore.

Opscore 3.9 delivers several new capabilities to end-users:

ITO33 is Sponsor of Volatility and Tail Risk Investing conference

6 April 2017, London

ITO33/Kite Surf 1st VOLATILITY SUMMIT: Everything you always wanted to know about Volatility but were afraid to ask

Among the various issues that will be covered, here is a foretaste:

31 RUE FROIDEVAUX 75014 PARIS, FRANCE

31 RUE FROIDEVAUX 75014 PARIS, FRANCE

If you prefer send us an e-mail

If you prefer send us an e-mail